Public Sector Banks Outperform Private Banks in Profits, Struggle to Hold Ground in Market Share

Public sector banks post record profits and improved asset quality, yet continue to lose market share to private banks amid staffing gaps and governance concerns.

Author: Neha Bodke

Published: June 17, 2025

Public Sector Banks (PSBs) in India have posted historic financial results in FY 2025, achieving significant progress across profitability, asset quality, and operational efficiency. However, their market share in both deposits and credit continues to shrink, raising urgent concerns over their long-term positioning in the country’s banking landscape.

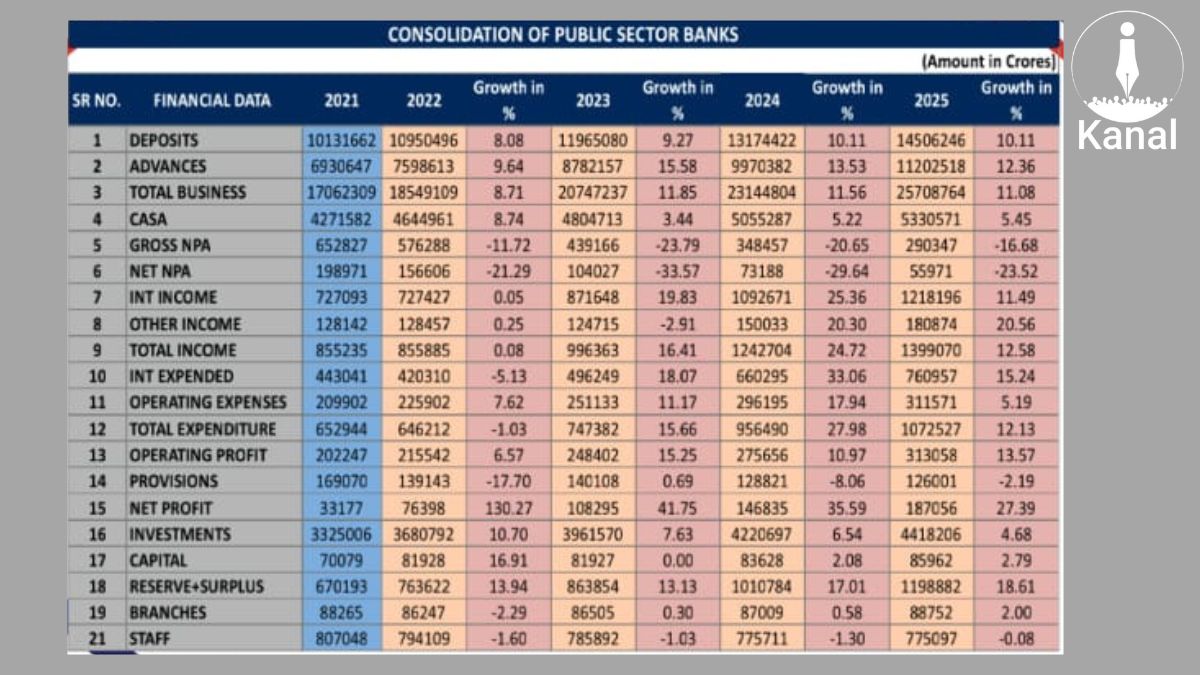

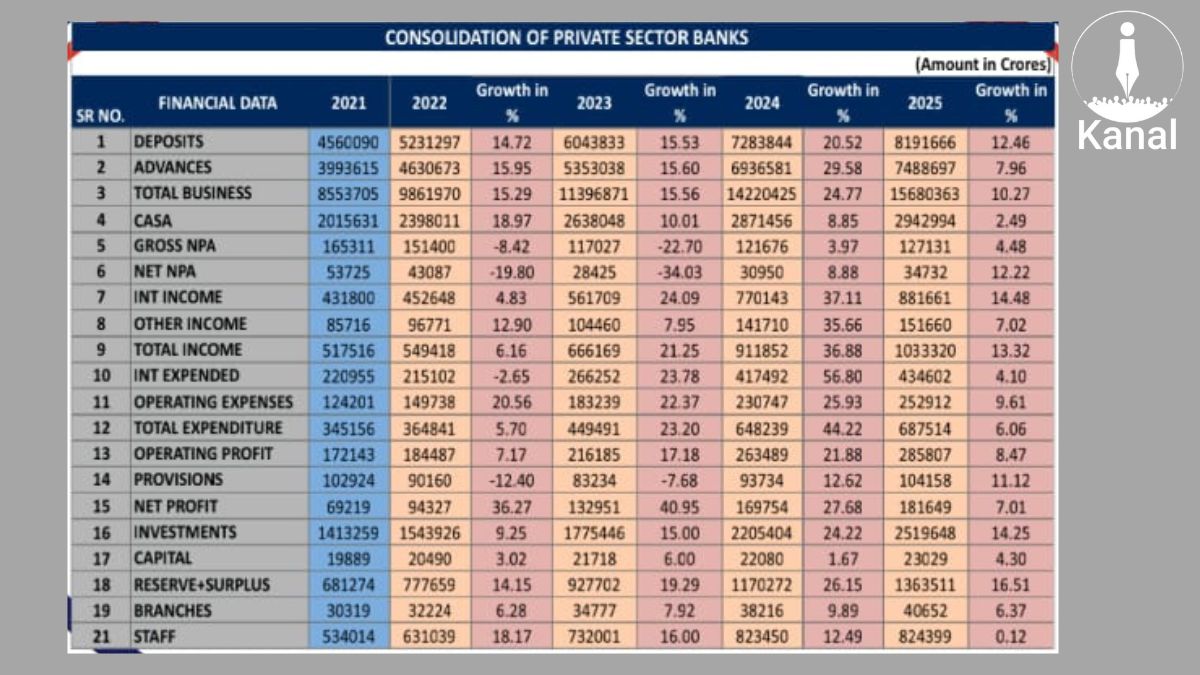

According to the Banking Statistics 2021–2025 booklet published by the All India Bank Employees Association (AIBEA), the total net profit of all public sector banks in FY25 stood at ₹1.87 lakh crore, marking a 27.39% increase over the previous year. In contrast, private sector banks registered a total profit of ₹1.81 lakh crore, with a more modest growth rate of 7.01%.

The trend marks a significant shift in profitability dynamics. Public banks, which were previously seen as lagging in earnings, have now matched and even outpaced private peers in absolute profit numbers for the financial year ending March 2025.

PSBs Achieve Major Gains in Asset Quality

PSBs also achieved substantial reductions in bad loans. The gross NPAs fell from ₹6.52 lakh crore in FY21 to ₹2.90 lakh crore in FY25, while net NPAs declined from ₹1.98 lakh crore to ₹55,971 crore over the same period. This indicates both an improvement in recovery mechanisms and better credit discipline.

On a percentage basis, gross NPAs of public sector banks fell from 9.42% in FY21 to 2.59% in FY25, and net NPAs from 3.07% to just 0.51%, a remarkable improvement in asset quality.

Private banks also saw improvement, but not as sharply. Gross NPAs in private sector banks stood at ₹1.27 lakh crore in FY25 compared to ₹1.65 lakh crore in FY21. Their net NPAs were ₹34,732 crore, down from ₹53,725 crore in 2021.

Speaking to Kanal on the nature of recent bank profits, Devidas Tuljapurkar, senior union leader and Joint Secretary of AIBEA, said, “The current profits are largely driven by reversal of earlier provisions, not by increased business volume or service-led income. Without volume-led growth, this profitability isn’t sustainable.”

Advertisement

AIBEA’s consolidated data shows PSBs leading in profitability and asset quality.

AIBEA’s consolidated data shows private banks continue to gain market share in deposits and advances.

Operating Profit and Total Business Surge

Public banks’ operating profit reached ₹3.13 lakh crore in FY25, up from ₹2.02 lakh crore in FY21 with a compound annual growth rate (CAGR) of over 11%. Total business (deposits plus advances) also saw robust growth, increasing from ₹170.62 lakh crore in FY21 to ₹257.08 lakh crore in FY25, registering an 11.08% CAGR.

Despite these strong operational numbers, market share continues to decline. PSBs’ share in total deposits fell from 68.96% in FY21 to 63.91% in FY25, while in total advances, their share decreased from 63.44% to 59.93% over the same five-year period.

Private sector banks, particularly large new-generation banks like HDFC Bank, ICICI Bank, Axis Bank, and Kotak Mahindra Bank have aggressively gained ground through branch expansion, technology, and customer-centric models.

Staffing and Resource Strain Highlighted

The booklet also includes concerns over staff shortages and workload pressures. Total staff strength in PSBs declined from 8.07 lakh in FY21 to 7.75 lakh in FY25, a net loss of over 32,000 employees in five years, even as business volume and customer load increased.

Additionally, PSBs added just 1,487 branches between FY21 and FY25, indicating limited physical expansion compared to private players. Many PSBs also reported increasing reliance on outsourcing and contractual staffing, which has implications for service quality and employee morale.

“The government claims to grant autonomy to banks, but at the same time, bureaucratic instructions to halt clerical and sub-staff recruitment choke operational capacity. Without adequate manpower, public banks simply cannot deliver,” Tuljapurkar noted.

“Excessive reliance on outsourcing and contractual employment invites serious operational risks. Many fraud cases today have roots in such unregulated staffing practices,” he added.

While staffing is a pressing concern, deeper systemic challenges related to governance and digital infrastructure further hinder PSBs’ efficiency.

“The IT infrastructure in many PSBs lags behind — software bottlenecks, underpowered hardware, and capacity issues prevent banks from operating at full throttle. They’re told to perform on par with private players but denied the tools to do so,” Tuljapurkar said.

Corporate Governance Concerns

Experts also point to weakening corporate governance as a major barrier to PSB growth. Many banks are operating with board positions vacant, undermining decision-making.

“Nearly 50% of board positions are vacant. Legally, there should be representation from depositors, agriculture, legal fields, etc. But in some banks, only five of the 14 board members are active, mostly government nominees or long-time directors. Audit committees, in some cases, aren’t even operationalised,” said Tuljapurkar.

The financial numbers demonstrate that PSBs remain crucial and high-performing pillars of India’s banking sector. Their role in financial inclusion, credit access to rural and priority sectors, and crisis-time stability remains unmatched. However, their shrinking market share, reduced workforce, and limited capital support demand urgent policy focus.

As the government explores structural reforms, experts and stakeholders will be closely watching whether these banks are empowered to expand, or sidelined in favor of aggressive privatisation.

Advertisement

No comments yet.