Public Sector Banks’ Losses Spark Questions on Accountability, ₹12 Lakh Crore Loan Written Off

Public Sector Banks wrote off ₹12.08 lakh crore of loans in 9 years, 1,629 wilful defaulters still owe ₹1.62 lakh crore. Experts question accountability, recovery, and corporate favoritism.

Author: Neha Bodke

Published: July 25, 2025

Public Sector Banks (PSBs) in India have written off a staggering ₹12,08,882 crore between 2015-16 and 2024-25, according to an official Finance Ministry reply in the Rajya Sabha. These write-offs are loans removed from bank books after being declared unrecoverable even as the liability technically remains.

1,629 Wilful Defaulters Still Owe ₹1.62 Lakh Crore

The same Finance Ministry reply revealed that 1,629 borrowers, each with defaults over ₹1 crore, have been declared wilful defaulters as of March 2024. The total amount they owe is ₹1,62,938 crore.

Former General Secretary of All India Bank of India Officers Confederation (AIBOC), Thomas Franco said to Kanal, “These defaulters have the capacity to pay but don’t. Yet the system helps them. Assets are sold cheap to other corporates, like Anil Ambani’s to Mukesh Ambani and recovery is just 1% or 5% also Videocon’s to Anil Agarwal and recovery is just 5%. This is not reform, it’s corporate benefit.”

He added that such sales through insolvency proceedings are often facilitated by retired judges or brokers, who act as insolvency professionals, creating a collusive ecosystem where corporate buyers benefit while banks and depositors lose.

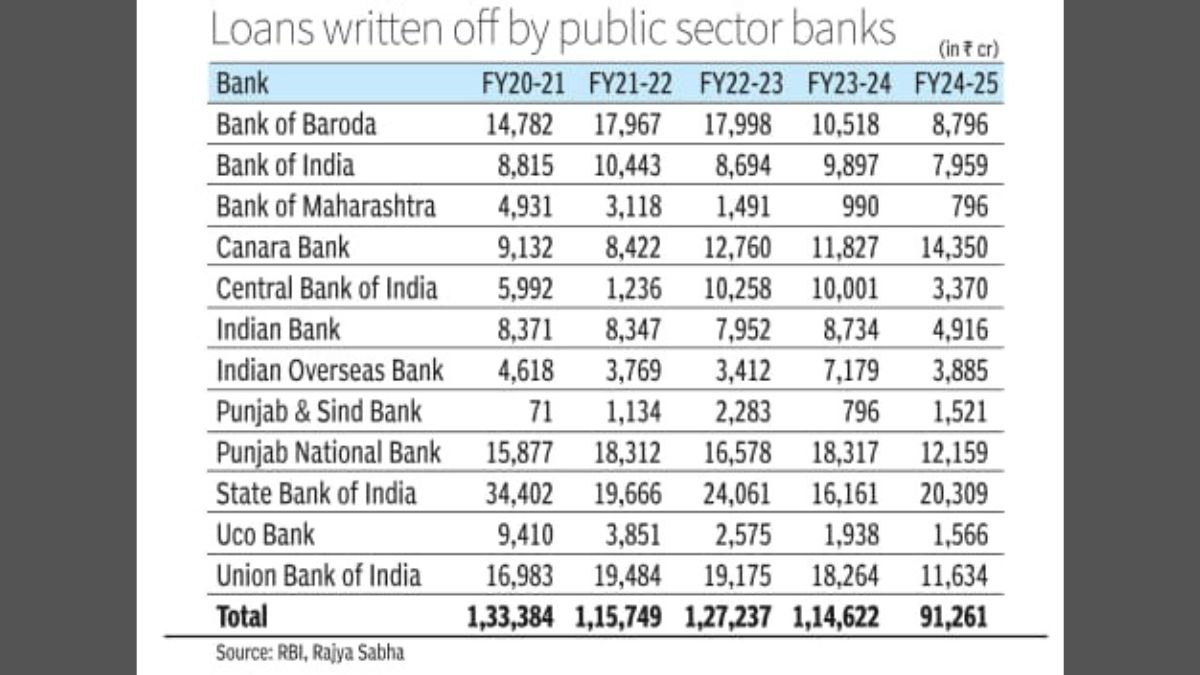

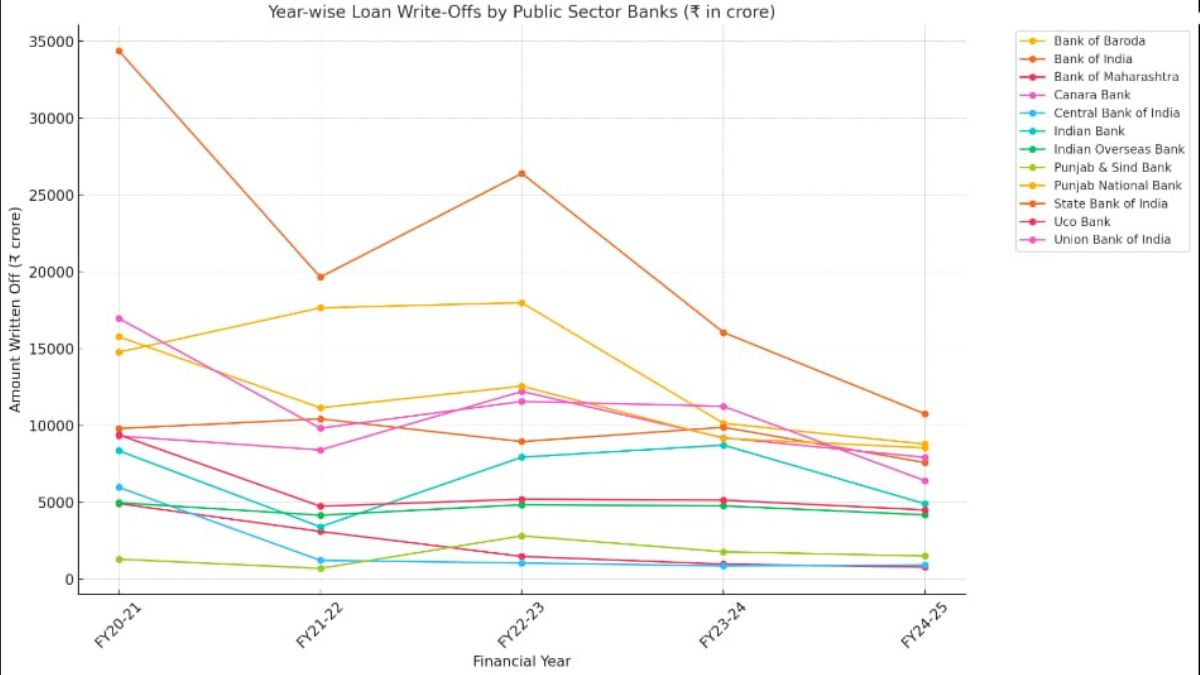

Bank-Wise Losses: SBI Tops the Chart

Among PSBs, the State Bank of India (SBI) leads the chart with ₹1.06 lakh crore in write-offs, nearly 9% of the total.

While other bank-wise data wasn’t detailed in the reply, similar trends exist across large PSBs like PNB, Bank of Baroda, and Union Bank.

Advertisement

Courtesy: RBI

Are Write-Offs Waivers?

The government clarified:

Advertisement

- Write-offs are not waivers

- Banks make provisioning as per RBI rules

- Recovery continues post write-off

However, Franco strongly disagrees with this narrative, “Recovery remains around 15-20% overall. There are laws like Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act (SARFAESI) and Insolvency and Bankruptcy Code (IBC) but delays and poor enforcement kill results. Cases drag for years. Recovery is negligible. Parliament itself admitted it benefits corporations more than banks.”

He further cited the IBC’s 180-day limit, which in reality averages over 480 days now, and noted how many insolvency professionals were removed from approved lists due to malpractice.

While the Vice President of Bank of Employees Federation of India (BEFI), C P Krishnan said to Kanal, “In 10 years, banks have written off ₹21 lakh crore. Just ₹3.3 lakh crore has been recovered under IBC, and the government admits that only 12–15% of total write-offs are ever recovered. Worse, RBI allows even wilful defaulters to get fresh loans after a cooling period.”

Tools for Recovery, But Do They Work?

The government cites mechanisms for recovering bad loan:

- Debt Recovery Tribunals (DRTs)

- SARFAESI Act

- National Company Law Tribunal (NCLT)

- Enforcement under PMLA & FEMA (₹15,870 crore total seized assets)

However, Thomas Franco argues that the problem lies at the root - in how the loans are sanctioned. mechanisms and points, “These loans were granted without proper collateral, based purely on inflated projections and pressure from the top. There’s political interference, and banks are often forced to lend. Later, recovery becomes impossible. The system is rigged against the public.”

The Bigger Picture: Corporate Privilege vs. Public Accountability

“Agricultural borrowers don’t get second chances like corporations do. This entire framework NCLT, IBC, write-offs is built to protect corporations at the cost of taxpayers and depositors,”Franco's remarks are a direct indictment of a system where the rich default without consequences, while the banking workforce and public funds bear the burden.

According to the experts, from write-offs to wilful defaults, poor recoveries to staffing pressures, this is not just a banking crisis, but a systemic rot. Without radical transparency, political will, and real accountability, the Indian banking sector risks becoming a conduit for corporate write-offs rather than a pillar of national development.

Advertisement

No comments yet.